Unexpected expenses have a way of appearing at the worst possible moments. A car suddenly breaks down on the way to work. A family member needs medical care. A household appliance stops working. A company announces layoffs. Life rarely sends warnings before financial problems arrive.

For many people, emergencies become crises not because the event itself is impossible to handle, but because there was no financial cushion waiting in the background.

That is where emergency savings becomes important.

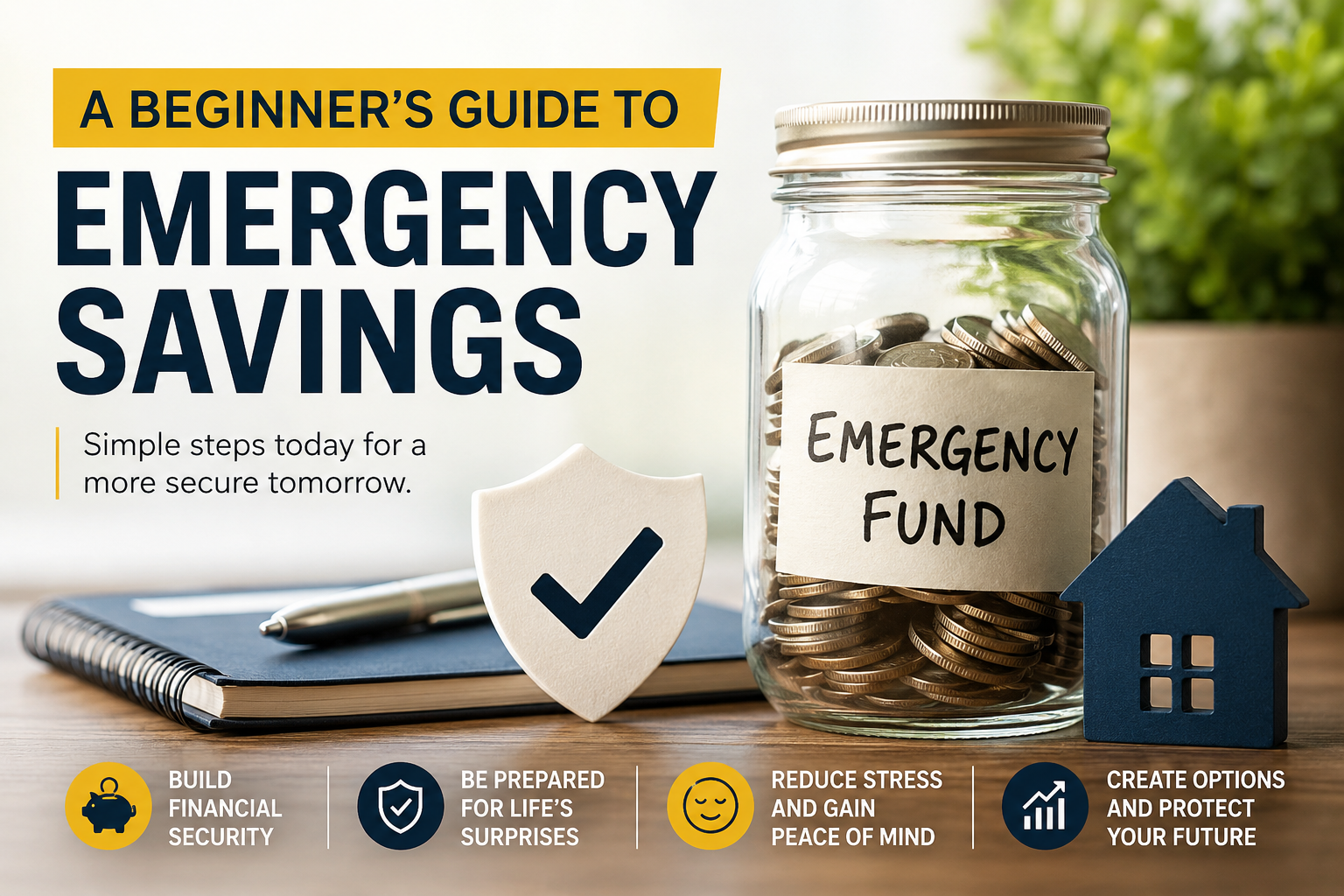

An emergency fund is not a luxury reserved for wealthy people. It is one of the most important financial tools anyone can build, regardless of income level. It provides protection during difficult times and creates a sense of stability that many people underestimate until they need it.

If you are just beginning your financial journey and have no idea where to start, this guide will walk you through everything—from understanding what emergency savings actually means to building your first safety net step by step.

What Is an Emergency Fund?

An emergency fund is money set aside specifically for unexpected and necessary expenses.

Its purpose is simple: to help you survive financial shocks without immediately falling into debt.

Unlike regular savings, emergency savings is not meant for shopping, vacations, gadgets, or planned purchases. It exists for situations that genuinely disrupt your life.

Think of it as a financial airbag. You hope you never need it, but you will be thankful it exists when problems happen.

Examples of true emergencies include:

- Job loss

- Medical emergencies

- Urgent home repairs

- Major car repairs

- Emergency travel because of family situations

- Sudden income interruptions

- Natural disasters or unexpected events

However, many expenses that people call emergencies are actually not emergencies.

Examples include:

- Buying concert tickets

- Holiday shopping

- Upgrading your smartphone

- Flash sales

- Impulse purchases

- Last-minute vacations

Learning the difference matters because emergency funds lose their purpose when used for wants rather than needs.

Why People Often Ignore Emergency Savings

Many people understand saving is important but still delay starting.

There are several reasons.

Some believe emergencies only happen to others.

Some feel their income is too small.

Others rely heavily on credit cards or loans and assume they can borrow if problems appear.

Many simply were never taught financial planning.

There is also a psychological reason.

Humans naturally prioritize immediate rewards over future protection.

Buying something enjoyable today feels more satisfying than preparing for a problem that may or may not happen months from now.

But financial emergencies eventually happen to almost everyone.

Preparation matters more than prediction.

The Real Cost of Not Having Emergency Savings

People often focus only on the money side of emergencies, but the effects usually spread into many areas of life.

Debt traps

Without emergency savings, people frequently turn to:

- Credit cards

- Payday loans

- Personal loans

- Borrowing from family and friends

The problem is that emergencies do not disappear after borrowing.

Now the emergency becomes a debt problem too.

High-interest payments can turn a temporary financial setback into years of repayment.

Emotional stress

Financial pressure affects mental well-being.

People experiencing financial insecurity often report:

- Constant anxiety

- Difficulty sleeping

- Stress-related health problems

- Relationship conflicts

- Persistent worry

Money problems can quietly affect nearly every part of life.

Delayed goals

Without savings, future plans often get pushed back.

Buying a home.

Starting a business.

Travel goals.

Retirement planning.

Investments.

Emergencies can interrupt progress when there is no safety net.

How Much Emergency Savings Should You Aim For?

Many financial experts recommend saving three to six months of essential living expenses.

The reason is straightforward.

If income suddenly stops, you still need money for:

- Housing

- Food

- Utilities

- Transportation

- Healthcare

- Basic obligations

However, beginners often become discouraged because six months sounds overwhelming.

Instead of focusing immediately on large goals, break the process into stages.

Stage 1: Save your first emergency amount

Aim for a small target:

₱5,000–₱20,000 or whatever amount feels realistic.

This creates immediate protection against small emergencies.

Stage 2: Save one month of expenses

This gives breathing room if something unexpected occurs.

Stage 3: Save three months of expenses

Now your financial stability becomes stronger.

Stage 4: Work toward six months or more

People with unstable work, freelance income, or dependents may benefit from larger emergency funds.

Progress matters more than perfection.

A small emergency fund is still far better than having none.

Calculate Your Essential Monthly Expenses

Before building an emergency fund, determine your survival expenses.

Ask yourself:

“If I temporarily lost income tomorrow, what expenses would still continue?”

Include:

Housing:

- Rent

- Mortgage

Utilities:

- Electricity

- Water

- Internet

Food:

- Groceries

Transportation:

- Fuel

- Commuting costs

Healthcare:

- Medicine

- Insurance

Debt payments

Now separate needs from wants.

Needs:

- Food

- Shelter

- Utilities

- Transportation for work

Wants:

- Multiple subscriptions

- Frequent restaurant meals

- Luxury purchases

- Upgrades

Understanding this difference helps you identify realistic emergency targets.

Why Starting Small Is Better Than Waiting

One of the biggest financial myths is:

“I’ll save when I earn more money.”

Unfortunately, income alone does not guarantee savings.

As income rises, spending often rises too.

This is called lifestyle inflation.

Someone earning twice as much may still struggle financially if expenses increase at the same pace.

Small habits often create larger changes.

Examples:

- Save spare change

- Transfer ₱50–₱100 daily

- Skip unnecessary purchases occasionally

- Set weekly savings goals

Consistency matters more than dramatic effort.

Small actions repeated regularly become powerful over time.

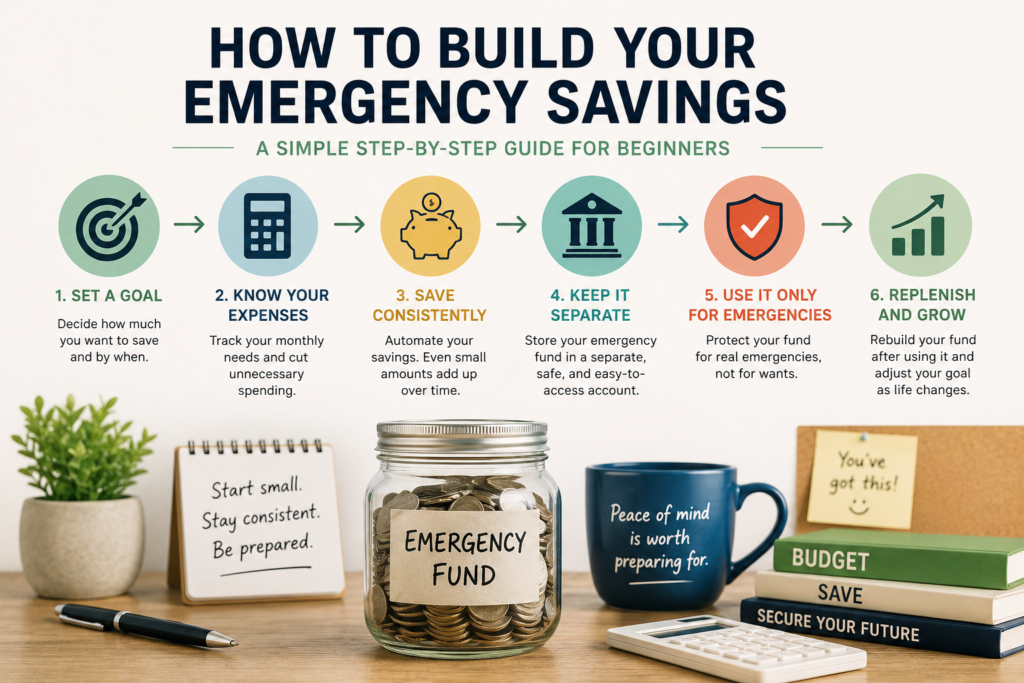

Step-by-Step Plan for Building Emergency Savings

Step 1: Open a separate savings account

Keeping emergency money separate reduces temptation.

You can choose:

- Traditional banks

- Digital banks

- High-yield savings accounts

The goal is accessibility without making withdrawals too easy.

Step 2: Set a specific target

Instead of saying:

“I want to save money.”

Say:

“I want to save ₱20,000 in eight months.”

Specific goals are easier to measure and follow.

Step 3: Create a basic budget

Use a simple formula:

Income

Minus expenses

Minus savings target

A budget is not punishment.

A budget simply gives instructions to your money.

Step 4: Automate savings

Automation removes decision-making.

Possible methods:

- Automatic transfers

- Payroll deductions

- Scheduled deposits

This follows the principle of paying yourself first.

Instead of saving what remains after spending, save before spending begins.

Step 5: Increase contributions gradually

As income grows, increase savings contributions.

Even small increases matter.

Practical Ways to Find Extra Money

Many people assume they have nothing left to save.

But small spending leaks can quietly drain finances.

Examples include:

- Unused subscriptions

- Excessive food delivery

- Impulse purchases

- Forgotten memberships

Review spending for one month.

Many people become surprised by where money actually goes.

Try short-term challenges:

- No-spend weekends

- Budget weeks

- Tracking every expense

Additional income opportunities can also help:

- Freelance work

- Online tasks

- Selling unused items

- Tutoring

- Side projects

Emergency savings does not require huge sacrifices.

Sometimes small adjustments are enough.

Where Should You Keep Emergency Savings?

Emergency funds should have four qualities:

Safe.

Accessible.

Separate.

Low risk.

Possible options include:

Traditional banks:

Reliable and familiar.

Digital banks:

Often offer higher interest rates.

High-yield savings accounts:

May grow slightly faster while staying accessible.

Money market accounts:

Useful in some situations.

Avoid placing emergency savings into high-risk assets.

Examples:

- Stocks

- Cryptocurrency

- Speculative investments

- Long lock-in accounts

Emergency money exists for emergencies.

If the market falls right when you need funds, access becomes a problem.

Common Beginner Mistakes

Waiting for perfect timing

Many people wait for a salary increase.

Start with what you have.

Setting unrealistic goals

Trying to save huge amounts immediately can create frustration.

Build gradually.

Using emergency funds for non-emergencies

Ask:

“Is this unexpected, urgent, and necessary?”

If not, think carefully.

Keeping funds too accessible

Money sitting beside everyday spending accounts may disappear quickly.

Stopping after reaching a small goal

Financial needs change.

Continue building.

What Happens After Reaching Your Goal?

Emergency savings is a foundation, not the final destination.

Once your fund becomes stable, focus on other financial priorities:

- Paying high-interest debt

- Investing

- Retirement planning

- Insurance

- Long-term goals

Remember to replenish emergency savings after using it.

Life changes.

Expenses change.

Review your emergency fund regularly.

Final Thoughts

Emergency savings is not about becoming rich.

It is about creating breathing room.

It is about reducing fear.

It is about giving yourself choices during difficult moments.

Many people delay saving because they believe they need large amounts of money to begin.

They do not.

The first few hundred pesos matter.

The first small deposit matters.

The first financial habit matters.

The best time to prepare for emergencies is before they happen.

Even small amounts saved today can protect your future tomorrow.